Exploring the Evolving Landscape in APAC Dermocosmetics Market

Asia Pacific is the largest region in beauty and personal care in 2021. The region is predicted to account for at least two thirds of beauty and personal care absolute value gains globally from now until 2026. Rising disposable incomes, rapid e-commerce acceleration pre-pandemic, substantial consumer appetite for skin care, and emerging demand for lower-penetrated categories of colour cosmetics and fragrances characterise much of the growth in the region.

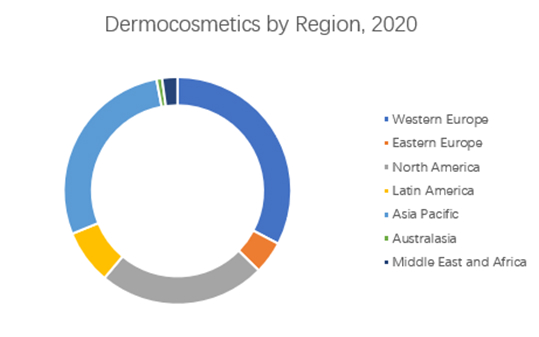

Asia Pacific is also the second largest region, behind Western Europe, in dermocosmetics, which Euromonitor International defines as therapeutic-positioned products that promote health and beauty of skin and hair by combining properties of cosmetics products (including but not limited to cleansing, moisturising, beautifying) and those of dermatologicals (treating skin and/or scalp concerns). In 2018, Asia Pacific surpassed North America as the second most valuable dermocosmetics region and since then, has grown steadily, particularly within skin care.

Source: Euromonitor’s Passport Database, 2020

APAC consumers’ emphasis on skin care contributes to dermocosmetics growth in Asia Pacific

According to Euromonitor International’s Voice of the Consumer: Beauty Survey in 2021, approximately one in five (19{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5}) APAC consumers have sensitive skin concerns, driven by stressful lifestyles, pollution and inappropriate usage of products. The pandemic outbreak further has propelled the development of skin health awareness amongst consumers and is driving demand for products with proven efficacy and a background in clinical research. Pandemic-driven wellness trends contributed to consumer behaviour changes that helped to generate healthy high-single digit growth in dermocosmetics in the region in 2020, which Euromonitor International expects to continue expanding in 2022 and beyond.

China, Japan, and South Korea are the three largest dermocosmetics markets in the region. Together, they account for 24{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5} of dermocosmetics sales globally; they also rank within the top 10 beauty and personal care markets, as of 2020. Aside from those top three markets, Hong Kong and India have also achieved high single-digit or low double-digit growth in dermocosmetics historically, driven by dermocosmetics facial care and bath and shower in Hong Kong, and dermocosmetics baby and child-specific products in India. Overall, the pandemic has not slowed down demand for dermocosmetics in the region; out of the top 10 markets for dermocosmetics, every region posted gains in 2020 except for Japan, Hong Kong, and to a lesser extent, Vietnam.

Source: Euromonitor’s Passport Database, 2020

The dominance of skin care in dermocosmetics is evident in two different ways. First, skin care accounts for the bulk of sales for dermocosmetics, both globally and in the leading dermocosmetics markets in Asia Pacific. Second, the positioning of skin care brands as having dermocosmetic features is communicated the most by skin care players than in other beauty categories. According to Euromonitor International’s Via Online Pricing Sample, skin care comprises the highest proportion of online SKUs tagged with the attribute “dermocosmetics” among the top 10 dermocosmetics market in Asia Pacific in 2021.

Source: Euromonitor’s Via Online Pricing Sample, 1 January 2021 to 31 December 2021. *Philippines and Vietnam are not tracked in Via and were excluded, despite ranking within the top 10 dermocosmetics markets in Asia Pacific.

At a country level, the dermocosmetics positioning within baby and child-specific products is more emphasised online in India than it is in other markets. Across the top 10 markets, brands with a dermocosmetics positioning lack penetration of deodorants and oral care (0.7{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5} of SKUs in both categories), which may bode well for players that wish to fill a niche in the market.

Medical-level skin repair products gaining traction across Asia Pacific

Cosmetic surgery is becoming increasingly popular amongst Asian consumers, especially millennials and Generation Z urban dwellers. The trend originated from developed markets such as Japan and South Korea and gradually swept across Mainland China and ASEAN markets, and even nurtured many online consultation APPs such as SoYoung and Gengmei, which made cosmetics surgery a more approachable beauty solution for consumers. Such beauty procedures range from hyaluronic acid injections to botulinum toxin injections, to more complicated ones such as V-line jaw and prominent cheekbones.

The prevalence of cosmetic medical procedures spontaneously drives up the demand for “aftercare” products, including but not limited to repairing facial masks, ampoule and sprays, with usually accompany products with a dermocosmetics nature. These products are usually launched by companies with laboratory backgrounds and are recommended by beauty clinics and doctors to accelerate skin repair after medical procedures.

According to Euromonitor International’s Voice of the Consumer: Beauty Survey, 29{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5} of Chinese consumers have used dermocosmetics skin care or hair products following a doctor’s consultation, compared with the global average of 23{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5}, demonstrating that dermocosmetics brands with clinic/laboratory support are extremely appealing to Chinese consumers. In China, popular aftercare solutions tend to be masks with medical device certification which implies a stricter production environment and quality check, ingredients with fewer additives and proven efficacy with clinical trials. Hyaluronic acid and collagen are the key ingredients of such products, usually with a pitch for skin barrier repair; the former focuses on water replenishment and the latter on anti-ageing.

Domestic brands better echo consumers’ dermocosmetics needs in China

In Mainland China, homegrown brands are leveraging the national wave supported by rising culture confidence and preference towards local brands to reach new heights. Consumers’ perception towards “Made-in-China” has gradually evolved from past stereotypes of “low quality with cheap price” to “made with cutting-edge technology and value for money”. Many domestic enterprises have illustrated this point through strong R&D capabilities and deeper understanding of demands from local consumers.

For example, domestic enterprise Bloomage Biotech is one of the largest hyaluronic acid suppliers in the world. Leveraging its advantages in the medical beauty industry, Bloomage Biotech launched several B2C brands locally, including BIOHYALUX and QUADHA, which both feature its high potency hyaluronic acid and advanced extracting technology. BIOHYALUX HA AQUA Single Use Essence uses INFIHA-HYDRA technology to boost hyaluronic acid absorption; and hero product Single Use Salicylic Acid Anti-acne Essence from QUADHA treats acne-prone skin with salicylic acid while repairing skin barrier with oligopeptide and hyaluronic acid.

Pharmaceutical and dermocosmetic synergy contributes to greater trust and innovation in South Korea

Local pharmaceutical companies with a strong reputation in dermatologicals also perform well, as consumers are more likely to trust the efficacy of ingredients from suppliers with a medical heritage. In South Korea, for example, DongKook Pharmaceutical Co Ltd produces Madecassol, the leading topical germicidals/antiseptics brand that commands a 41{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5} market share in 2021. The parent company incorporated the essential ingredient found in Madecassol in its dermocosmetics line, Centellian 24, with the launch of Madeca Cream, known for its moisturising properties to repair damaged skin.

Competitor brand Fucidin, under Dong Wha Pharmaceutical Industrial Co Ltd, recently launched Fusid Cream using a strategy similar to the one employed by Madeca Cream. Retailers in South Korea reinforce this messaging of ingredient efficacy by offering substantial information through product description and consumer feedback for consumers. Companies that can leverage the pharmaceutical side of their business to innovate within dermocosmetics have an obvious advantage over other players, given that consumer trust and familiarity is already present.

Source: Euromonitor International’s Via Online Pricing Sample, 19 January 2022

COVID-19 crisis continues to propel dermocosmetics in Japan

Increasing numbers of Japanese consumers are experiencing unstable skin conditions such as acne and weaker skin barriers due to the unprecedented changes brought about by COVID-19. Local dermocosmetics brand Curel unveiled a new star product in 2020 – The Curel Deep Moisture Spray, which is a quasi-drug product that provides moisture to both the face and body for consumers who suffer from sensitive and dry skin. The product features new ceramide care technology and an anti-inflammatory agent to prevent irritated skin.

It is also increasingly evident that drugstore chains are actively collaborating with leading beauty groups to co-launch dermocosmetics. For example, Matsumoto Cocokara & Co in Japan co-developed with KOSE group to launch the first private label skin care brand RECiPEO in 2021, targeting sensitive and dry skin. Furthermore, the pandemic has also raised awareness of skin health in Japan, including skin barrier enhancement and protection against UV rays, pollen and PM2.5. D program from local behemoth Shiseido Group designs all products to be hypoallergenic based on 50 years of delicate skin research in Japan.

Digital marketing the key to success

Beyond launching on established major online platforms such as Tmall, JD.com and WeChat e-store, many fast-growing dermocosmetics brands have been leveraging the rising trend of short-video APPs such as Douyin and Kuaishou, and even sites popular with Generation Z, namely Bilibili (or B Station) which was initially famous for sharing anime and comic video content, but recently entered the mainstream in beauty marketing by featuring make-up tutorials, unboxing videos and product reviews by KOLs.

Similarly, brands are usually highly active on social e-commerce platforms such as RED and Weibo, which enable brands to leverage the influence of KOLs and KOCs (key opinion consumers) to build brand awareness and increase trials. Livestreaming continues to play a vital role in driving sales, and accounts for a larger share of brand revenue in 2021. For example, sales from livestreaming comprises over 80{adb1ce361e4d115852a5ecc77da1fcd21e68b5d23904b1abbfd33825d7fe0fb5} of Dr.Yu’s total sales.

The online marketplace is an important channel for skin care in Asia Pacific, while its potential will continue to be unleashed over the forecast period. It has become increasingly evident that dermocosmetics brands that recorded dynamic growth in recent years have realised the importance of e-commerce and made greater efforts to engage with consumers by utilising various digital marketing tactics. In this way, these dermocosmetics brands are able to break through the limitation of offline channels and reach a broader range of consumers.

Future outlook

Consumers in Asia Pacific are showing increasing desire for safety, efficacy and transparency and demonstrating a greater preference for brands with a strong clinical and laboratory background. This would indicate strong potential for brands that can justify efficacy through a series of high-functioning ingredients and unique technology. Furthermore, online marketplaces will be the key battlefield for dermocosmetics brands, especially for those that aim to reach millennials and Generation Z. It is vital for brands to adopt various digital marketing tactics to drive brand awareness and make the connection with younger generations.

The skin care market in Asia Pacific is evolving relatively quickly, with fast-changing consumer attitudes and rapid new product launches. For example, “functional” skin care, which usually adopts high potency ingredients with concentrated formulas, is gaining increasing attention, especially amongst sophisticated consumers or “skintellectuals”, and could be a potential threat to brands with a dermocosmetics nature. Dermocosmetics is expected to witness fierce competition over the forecast period in Asia Pacific, momentum that beauty players in APAC can benefit from through formulation and ingredient innovation, digital marketing strategies, and by developing a strong consumer base.

For further insight, see this briefing.

https://www.euromonitor.com/article/exploring-the-evolving-landscape-in-apac-dermocosmetics-market